When you submit a personal loan application, lenders assess risk, affordability, and profile stability within minutes. Therefore, success depends on how clearly your financial position aligns with lending criteria rather than on intent or urgency. This article focuses only on actions that directly influence approval decisions and borrowing outcomes.

What Lenders Prioritise at First Review

Lenders follow a structured evaluation sequence, and early signals often decide the outcome before deeper checks begin.

At the first review stage, lenders focus on:

- Credit history quality and repayment discipline

- Income consistency and source reliability

- Existing debt obligations and monthly outflow levels

- Accuracy of personal, financial, and banking information

If these factors meet the lender's expectations, the application progresses smoothly. Weak signals at this stage usually lead to rejection or reduced loan offers.

Credit Profile Checks that Matter the Most

Your credit report forms the base of your instant personal loan application. Lenders treat it as a record of past borrowing behaviour and current financial exposure.

Before you apply for a personal loan, review your credit report to confirm:

- Personal details match official identity records

- Closed loans are not shown as active

- Repayments are reported accurately without incorrect delays

In addition, keep credit card utilisation controlled in the months before applying. Lower utilisation reflects disciplined credit usage and improves assessment outcomes.

Accuracy matters more than perfection during credit evaluation.

How Lenders Judge Affordability

Affordability assessment determines whether your income can support additional repayments without stress. Lenders rely on net income, not headline figures.

You should evaluate affordability using realistic numbers that include all fixed commitments. Hidden liabilities or inflated income declarations weaken credibility during verification. Using tools like a personal loan EMI calculator helps you understand repayment feasibility before submitting your application.

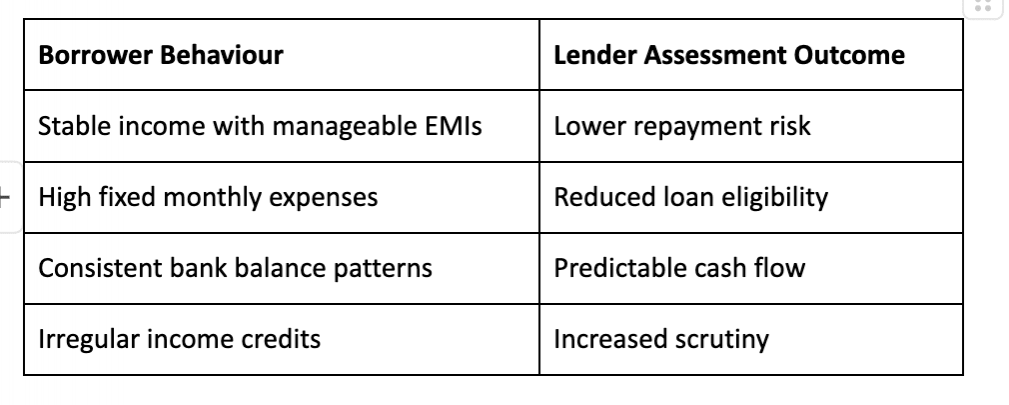

The table below shows how lenders interpret common affordability signals.

Clear affordability alignment strengthens approval confidence.

Choosing the Right Loan Amount

The amount you request influences both risk perception and approval probability. Lenders prefer precision over excessive borrowing.

You should match the loan amount to a defined requirement instead of adding buffers. Purpose-driven borrowing appears controlled and easier to service over time.

A well-calculated loan amount reduces repayment pressure and limits long-term interest exposure.

Documentation Readiness Checklist

Incomplete documentation remains a major cause of delays and rejections. Lenders expect consistency across all submitted records.

Before starting your application, confirm that:

- Identity and address details match across documents

- Income proofs reflect consistent earning patterns

- Bank statements show stable transaction behaviour

Preparing documents in advance improves processing speed and signals reliability.

Income Stability Signals Lenders Trust

Income stability plays a critical role in repayment forecasting. Lenders value continuity over short-term income increases.

If you recently changed jobs, applying after completing a reasonable tenure strengthens credibility. Frequent changes raise questions about repayment reliability.

For self-employed applicants, steady income across multiple periods improves lender comfort. Sudden income spikes without history often attract deeper verification.

Application timing matters more than income optimism.

Application Frequency and Credit Enquiries

Each personal loan application generates a credit enquiry. Multiple enquiries within a short span weaken your credit profile.

You should apply selectively after checking eligibility conditions carefully. A focused approach protects your credit standing and reflects financial control.

One prepared application carries more weight than several rushed attempts.

Repayment Tenure Selection Strategy

Repayment tenure affects monthly affordability and total repayment cost. Lenders observe tenure choice as a sign of financial judgement.

Short tenures reduce interest burden but increase monthly pressure. Longer tenures ease monthly outflow while raising overall repayment amounts.

You should select a tenure that balances comfort with cost efficiency. Balanced choices signal financial maturity. A well‑selected tenure for a 1 lakh loan demonstrates responsible planning and strengthens your overall credit behaviour.

Financial Behaviour Before Applying

Sudden financial changes before application weaken your profile. Lenders look for predictable behaviour over recent months.

Avoid these actions before applying:

- Large cash withdrawals

- Heavy credit card spending

- Taking new credit commitments

Stable financial patterns simplify assessment and strengthen trust.

Review Loan Terms Before Acceptance

Approval does not end responsibility. You should review interest structure, processing charges, and prepayment conditions carefully.

Clear understanding of repayment schedules helps you plan effectively and avoid unexpected costs. Informed acceptance supports long-term financial stability.

Conclusion

Successful personal loan applications depend on preparation, clarity, and disciplined financial behaviour. When your credit accuracy, affordability, documentation, and income stability align with lender expectations, approval becomes more predictable. A structured approach protects your finances and strengthens future borrowing capacity.