Oil prices dipped in early Asian trade Tuesday, but both U.S. and international crude futures held above $40 per barrel ahead of a meeting of major producers to discuss freezing output levels to rein in ballooning oversupply.

U.S. West Texas Intermediate (WTI) crude futures CLc1 were trading at $40.27 per barrel at 0059 GMT, down 9 cents from their last settlement.

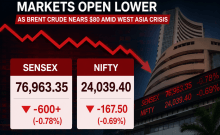

International Brent crude futures LCOc1 were at $42.70 a barrel, 13 cents below their last close but only 36 cents off their 2016-high reached the previous day.

Major oil producers from the Middle East and Russia, but excluding the United States, plan to meet in Qatar's capital Doha next Sunday. They will discuss measures to rein in ballooning oversupply which sees as many as 2 million barrels of crude produced every day in excess of demand, leaving storage tanks around the world filled to the rims with unsold and unwanted fuel.

Most analysts expect producers to freeze output around current output levels, which being beyond consumption and close to record levels would do little to address the glut.

"The potential risk for prices is for the downside as freezing output at current levels would be more of a symbolic act rather than a real market intervention. But you need to be open to surprises in this market," said Ric Spooner, chief market analyst at CMC Markets in Sydney.

While Spooner said that a production freeze would do little to address the immediate glut, he added that keeping key Middle East and Russian output around current levels might in the longer term lead to a more balanced market.

"There is demand growth, and production in the U.S. is falling, so if against that background there was a freeze, markets could get tighter at some stage," he said.

Analysts at Bernstein said that they expected global oil demand to grow at a mean annual rate of 1.4 percent between 2016 and 2020, versus annual growth of 1.1 percent over the past decade, adding that global demand would reach 101.1 million barrels per day (bpd) by 2020 from 94.6 million bpd now.

Looking further into the future, Bernstein said that world oil demand would likely peak in the 2030s.

"The world will reach 'peak demand' before 'peak supply'. Global oil demand is likely to peak around 2030-35 at 108 million bpd."