Some investors today have become aware of NPS or the National Pension System. But a whole lot more already invest their money in PPF or Public Provident Fund. Convincing investors, who already use PPF, that NPS is a good option is much like telling Sachin Tendulkar fans that Virat Kohli is as good. Let's see what are the major differences between these two products, both of which can be used to build a retirement corpus. The best part is you can use both products to get pension.

Guarantee of returns – PPF, as we all know, is Mr Dependable. Why? Because PPF guarantees returns. People start investing in Public Provident Fund purely from a returns perspective. PPF gives 7.9 per cent at present. An individual can invest Rs 1.5 lakh per annum in PPF. The income is tax free. For anyone who is happy with a 7.9 percent return in a scenario where bank fixed deposits carry even lower interest rates, PPF makes sense. Plus, the interest income earned on a normal bank FD is taxable. Though PPF returns have been lowered over the years (it used to yield as high as 12 percent in 1999), PPF returns today must be in seen context of inflation. When inflation is 3-4 percent, the 7.9 percent from PPF when adjusted for inflation goes give you a good positive real rate of return. In contrast, when inflation was in double digits, the real rate of PPF return was probably negative even at 12 percent.

Coming to NPS, there is no guarantee of returns. There is no implicit or explicit minimum guaranteed return under NPS. In this system, NPS helps make equity and debt asset classes available under a single platform. There is also an option to switch between them with varying allocations. The life stage option in NPS automatically allocates funds between assets as one ages. Since your money is invested in market-linked instruments, there is no cap for returns. Equities or stocks can give great returns when held for the long term.

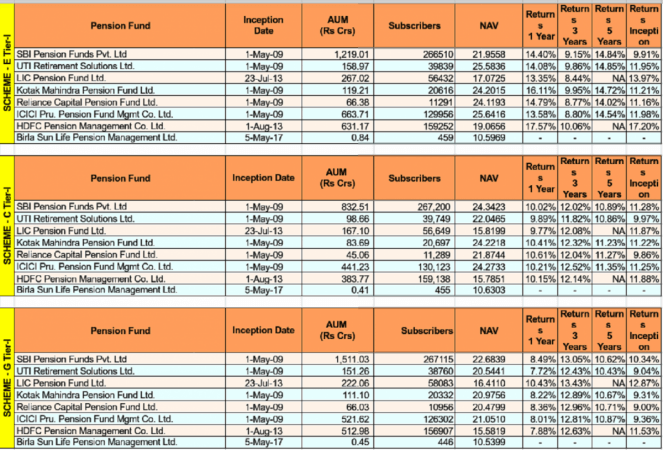

As per latest data from the NPS Trust, different NPS schemes have given between 9 to 17 percent since inception. The returns depend on how the fund managers use your money. But given that NPS is a government overseen scheme, fund managers can't do monkey business with your money and have to invest in a proper fashion adhering to various stringent norms.

In practice, returns from NPS could be far higher than PPF. But there is a 'if'. In case NPS returns are lower than PPF, you do not have any downside protection. So, for investors who value a guarantee much more, PPF is probably the best option. If you are not too obsessed with guarantees and are comfortable with market-linked returns, invest some money in NPS as well. There are no rules which state that you have to choose one over the other. In fact, if you combine both PPF and NPS you will be able to get good tax benefits that will lower your taxable income.

Freedom to use the corpus at maturity - PPF and NPS are both products that can be used to get to a retirement corpus. In India, only government sector people get pension. The rest of us, the private sector mortals, have no pension. This is why the common man and woman need to save for their own pension. Both PPF and NPS can help you in this regard. However, the approach is different.

In the case of PPF, the entire amount is given to you at the end of the maturity period. What you do with that money is nobody's lookout. You can spend the entire money for something totally unrelated to retirement. Nobody is bothered whether you use the money as a monthly pension source or use the interest at all. The liability of the PPF authority ends as soon as the maturity proceeds are transferred to your account.

In case of NPS, the approach is much more hands-on when it comes to maturity. Up to 60 percent of the maturity corpus can be withdrawn as lump sum on maturity in case of NPS at age 60. The remaining amount has to be compulsorily converted into annuity.

If the subscriber exits NPS before 60 years of age, then only up to 20 percent of the corpus can be withdrawn and rest has to be converted into annuity.

The compulsory annuity purchase is not without a valid reason. NPS is meant for giving you a pension, which is a regular income in your golden years (when you do not have any salary).

However, as we have seen in real life, senior citizens often end up as lender of the last resort to younger people in the family. It could be for down payment of the house your son/daughter will buy, or a part of the education money required for your grandkid's Ivy League degree. In many cases, the entire money for retirement could be used for a purpose that is not remotely linked to your post-retirement monetary needs. This is why compulsory annuity solves this problem partially. The amount that goes into purchase of annuity will automatically give a regular income stream.

Depending on how you view the compulsory annuity purchase component, you will be a advocate or opponent of NPS. The freedom to do anything with your money solely rests with you, but NPS puts a layer of protection that PPF doesnt.

Taxation angle - There is no escaping taxes, even if you are retired. Let us understand how the taxation system works for PPF and NPS.

PPF has a long maturity period of 15 years. The government has given EEE tax treatment. What does EEE mean? This means any investment in PPF will get exempt-exempt-exempt status in the three stages, namely at the time of contribution, on returns and on withdrawals. Even partial withdrawals, allowed only after 6 years, are exempt from tax. So, imagine: if you have accumulated Rs 40 lakh in PPF, the entire amount is tax-free.

PPF FEATURES

* Deposits can be made in lumpsum or in 12 installments.

* Nomination facility is available at the time of opening and also after opening of account.

* The subscriber can open another account in the name of minors but subject to maximum investment limit by adding balance in all accounts.

* Maturity period is 15 years but the same can be extended within one year of maturity for further 5 years and so on.

* Maturity value can be retained without extension and without further deposits also.

* Premature closure is not allowed before 15 years.

* Deposits qualify for deduction from income under Sec. 80C of IT Act.

* Interest is completely tax-free.

* Withdrawal is permissible every year from 7th financial year from the year of opening account.

* Loan facility available from 3rd financial year.

Is NPS also EEE? No. The NPS, unlike PPF, is subject to EET -- exempt, exempt and tax. This means contribution and accumulation are exempt from tax, but maturity amount is not. At maturity, 40 percent of withdrawal is tax exempt. Since the structure of NPS is such that you have to mandatorily buy an annuity with 40 percent of the corpus, the income from annuity will also be subject to tax as per applicable tax laws. Do remember that even if you deposit your entire tax-free PPF corpus in a bank FD, the interest income earned will also attract applicable tax.

So, is NPS an inferior instrument compared to PPF on tax? The answer depends on the amount of return earned. If your NPS contribution earns a higher return than PPF, you will end up with more money. For eg., you can deposit Rs 1.5 lakh maximum a year in PPF. If you do that for 15 years, you can get a corpus of Rs 46 lakh at maturity. In case your NPS return is 15 percent a year over a 15-year tenure, the same Rs 1.5 lakh yearly can lead to a higher corpus of Rs 84 lakh. All the government is asking is you is to pay some tax on the extra amount that you have earned in NPS. For investors who do not like paying tax, PPF is the only option. But do remember that the money you earn with PPF has to be deposited somewhere and if you earn any interest on it, the government will ask you to pay applicable tax.

Conclusion: PPF and NPS adopt different approaches to give you a post-retirement income. We suggest that you invest some money in NPS, once you have extinguished your annual limit in PPF. Depending upon your returns experience with NPS, you can increase or reduce your NPS contributions.