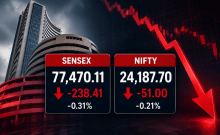

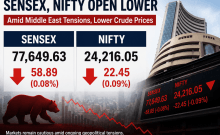

On a selling spree, foreign institutional investors (FIIs/FPIs) could further trim their holdings in Indian stocks fearing uncertainty after Prime Minister Narendra Modi's comments on "fair contribution to nation-building through taxes" last week.

Finance minister Arun Jaitley's denial on imposing long-term capital gains (LTCG) in any case did not matter on Monday when markets opened on a weak note and further extended their losses.

FM Arun Jaitley says time for India to have 'globally competitive' taxes

FIIs could read Modi's statement has the potential to raise "uncertainty" ahead of Budget 2017, says a brokerage.

"The recent clarification by the CBDT on the applicability of Section 9 (1) (i) of the IT Act, 1961 on incomes, which are deemed to accrue or arise from India and (2) the recent speech of the prime minister highlighting low tax on incomes from capital markets and increasing the same may create uncertainty about taxation of capital gains on equities and equity derivatives for domestic and foreign investors both, especially as the FY2018 Union Budget is due on February 1, 2017," Kotak Institutional Equities (KIE) said in a note on Monday.

The probability of double taxation could also arise in the wake of the twin developments.

"...several FPIs such as pension funds, SWFs will have a single dominant shareholder (with shareholding well above 5%) and as such, their gains may be taxable, if they do not qualify for any exceptions," KIE added.

"Similarly, the gains of investors of P-notes (registered as FPIs in India) may be taxable, as the income will be deemed to accrue or arise from India, if they do not qualify for any exceptions. We await more clarity on the same," the note further said.

The incidence of double taxation would not bother broad-based FPIs given their ownership pattern; most of them do not not have a single investor with more than 5 percent holding.

Income Tax provisions on deemed income

The rules governing income deemed to have accrued in India are specified in section 9 of the Income Tax Act, as reproduced below:

(1) The following incomes shall be deemed to accrue or arise in India :—

(i) all income accruing or arising, whether directly or indirectly, through or from any business connection in India, or through or from any property in India, or through or from any asset or source of income in India, or through the transfer of a capital asset situate in India.

Explanation 5: For the removal of doubts, it is hereby clarified that an asset or a capital asset being any share or interest in a company or entity registered or incorporated outside India shall be deemed to be and shall always be deemed to have been situated in India, if the share or interest derives, directly or indirectly, its value substantially from the assets located in India.

There are about 6,700 FPIs registered with the Securities and Exchange Board of India, according to the National Securities Depository Limited.