Standard & Poor's Ratings Services said on Friday that it has revised its outlook on India to stable from negative, citing the improved political setting of the country, which will offer a conducive environment for reforms, boost growth prospects and improve fiscal management.

This comes as a timely boost for Prime Minister Narendra Modi, who has been aggressively marketing his 'Make in India' slogan among global investors.

The rating agency affirmed the 'BBB-' long-term and 'A-3' short-term unsolicited sovereign credit ratings on Asia's third largest economy.

The Indian rupee, which was trading at a seven-week low, rebounded sharply after the release. USD/INR dropped to 61.01 from 61.61, which was its highest since 8 August.

The rupee was under pressure owing to the broad strength of the greenback, which is trading at a 4-year high as per a trade-weighted gauge against a basket of major currencies.

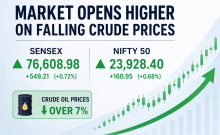

The main stock indices that were trading lower before the release made a sharp rebound after that. The NSE50 index ended 0.7% higher on the day.

Positives

"The ratings on India reflect the country's strong external profile, combined with its democratic institutions and free press, both of which underpin policy stability and predictability," S&P said in a press release.

"These strengths are balanced against the vulnerabilities stemming from the country's low per capita income and weak public finances."

The rating agency said India's external position is a key credit strength. The country has relatively little external debt and a much improved external liquidity position.

"We project that, at the fiscal year end of March 31, 2015, external debt net of external assets will be 6% of current account receipts," S&P said.

Central bank reserves well exceed public sector external debt, reflecting the public sector's ability to finance practically all of its borrowing requirement domestically, S&P said.

India's current account has improved in recent years after restrictions on gold imports and slower domestic investment demand, the rating agency noted. At the same time, the central bank rebuilt its foreign currency reserves to cover about 5.5 months of current account payments, it said.

"Although we expect the current account deficit to widen from its current low of 1.8% of GDP (as of March 2014) as investment picks up, gross external financing needs are likely to remain at or below the sum of CARs plus usable reserves in the next two to three years," S&P said.

India's well-entrenched democratic political system is another credit support. That, along with the country's mature and stable institutions (including free press) and system of checks and balances, has afforded India a long period of stability, the rating agency said.

"Although the paralyzing effect of legislative gridlock can blunt government effectiveness, our outlook revision indicates that we believe the current government's strong mandate will enable it to implement many of its administrative, fiscal, and economic reforms."

Constraints

India's low wealth level, as measured by per capita GDP, is one of the main constraints on the rating, said S&P.

"At $1,550, India's per capita GDP implies a narrow tax and funding base upon which the sovereign can draw to carry a given debt burden."

"We believe the current administration will remedy, to varying degrees, the growth impediments--policy paralysis, energy supply bottlenecks, and administrative obstacles," the rating agency said.

S&P said the government's actions will likely add momentum to the incipient cyclical upswing evident in the economy and projected real per capita GDP growth to reach 5% by next year, and per capita GDP to surpass $2,000 by 2017.

India's weak public finances are manifested in a long history of general government fiscal deficits, averaging 8.8% of GDP over the past 20 years, and an accumulated net general government debt stock of close to 70% of GDP, S&P noted.

"Prior governments have not been able to broaden India's revenue base (with general government revenue at about 21% of GDP, of which only half are taxes) or trim expenditure. India's budget is saddled with extensive subsidies for food, energy, and fertilizer."

The rating agency said it sees little foreign exchange or roll-over risk for the government as more than 90% of general government debt is denominated in rupees.

"Although real interest rates have been consistently negative, the interest cost on government debt amounts to almost a quarter of government revenues," the press release said.

"Fiscal flexibility is further constrained by the general shortage of infrastructure and basic government services."

Expectations

S&P said it expects the new administration to adhere to its stated fiscal consolidation programme, even as acknowledging that planned revenues may not fully materialise and subsidy cuts may be delayed.

"We expect improved fiscal performance in the medium term primarily from revenue-side improvements brought about by the planned introduction of a national goods and services tax

(GST) and administrative efforts to expand the tax base."

S&P projects net general government debt to decline to below 60% of GDP by the year ending March 2018, and with it, general government interest rate expense to just under 20% of revenues.

"A faster pace of deficit and debt reduction is unlikely in our view. Hence, we believe fiscal and debt metrics are set to remain key rating constraints for some time," the rating agency said.

"The stable outlook for the next 24 months reflects our view that the new government has both the willingness and capacity to implement reforms necessary to restore some of India's lost growth potential, consolidate its fiscal accounts, and permit the Reserve Bank of India to carry out effective monetary policy," S&P added.

The global rating company said it could raise the rating if the economy reverts to a real per capita GDP trend growth of 5.5% per year and fiscal, external, or inflation metrics improve.

"Conversely we may lower the rating if the government's structural reform agenda stalls such that economic growth does not accelerate, or fiscal and debt ratios fail to improve," it warned.