Before you apply for a credit card it is important to understand that managing repayments is an important part of using a credit card effectively. Whether you're planning a large purchase or looking to convert an existing transaction into EMIs, knowing your monthly instalment and the total interest payable can make your decisions clearer.A Credit Card EMI Calculator helps you do exactly that by giving you an instant estimate of your EMI amount, interest costs and repayment timeline. This tool makes it easier to compare different tenure options, plan your monthly budget and choose an EMI structure that fits your financial comfort.Here's how it works and why it can be helpful when planning upcoming expenses.

What is a Credit Card EMI Calculator?

Credit Card EMI Calculators allow you to estimate and calculate the potential Equated Monthly Instalment that you would pay when converting a credit card transaction into EMIs. It is most useful for larger purchases where spreading the cost across several months makes the expense easier to manage.

So how do EMIs work and how do they benefit you?

These calculators allow you to choose your principal amount, the applicable rate of interest as per your credit card, and the tenure that you prefer, to immediately understand your monthly instalment and the total cost of repayment.

To understand how EMIs work in practice, here's a simple example.

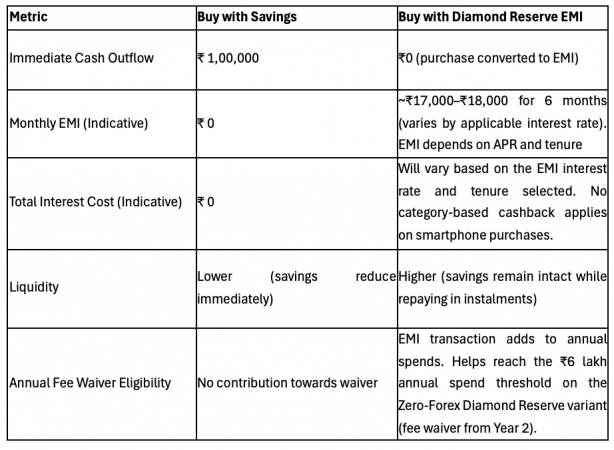

Ramesh lives in Mumbai and earns a monthly net income of ₹1,50,000. He has built steady savings habits and prefers to plan his expenses carefully. He wants to buy a new smartphone but is unsure whether to pay the full amount upfront or convert the purchase into EMIs. Using a credit card EMI calculator helps him compare both options clearly by showing:

- the EMI amount for different tenures

- the total interest he would pay

- how each option fits into his monthly budget

This gives him the clarity he needs to make a comfortable and well‑informed decision.

Here's the estimated example if Ramesh uses an IDFC FIRST Bank Diamond Reserve Credit Card.

For Ramesh, the biggest advantage of choosing the EMI option is that his savings remain untouched. By keeping his ₹4.5 lakh liquid, he maintains a financial buffer for any unexpected expense or emergency. The EMI amount also fits within his monthly budget, which means the repayment does not strain his cash flow.

Although EMIs come with an interest cost, they offer the flexibility to spread a large purchase over several months. For someone like Ramesh, who plans his finances carefully and prefers predictable monthly outgo, using an EMI can be a practical and comfortable approach.

What About the Liquidity Premium?

When deciding between paying upfront or choosing an EMI, Ramesh also needs to consider the value of keeping his savings intact. Using his savings would eliminate the interest cost, but it would also reduce his liquidity and stop that money from earning any potential returns. In a city like Mumbai, unexpected expenses, such as medical needs or urgent repairs, can arise without warning, so having cash available can be reassuring.

Choosing the EMI route allows Ramesh to preserve his savings while spreading the cost over a few months. As long as the EMI fits within his budget and he pays it on time, it can also help maintain a healthy credit profile. For someone who prefers financial stability and wants to keep a buffer for emergencies, opting for an EMI can be a practical choice.

Takeaway

Any financial decision deserves careful thought, whether it involves using your savings or choosing to repay through EMIs. For many people, EMIs act as a small premium for peace of mind, allowing large purchases to be spread over time while keeping savings intact.

Before you apply for a credit card, it helps to understand how the costs will play out month by month. Using a credit card EMI calculator can give you a clear estimate of instalments and interest, helping you make an informed choice that aligns with your budget and comfort.